Originally published on February 2, 2015 Last edited on August 7, 2017 By Michio Suginoo

[1] Shirakawa’s Remark: Paradox of Successful Monetary Policy

Does a successful monetary policy guarantee the stability of the economy? How would a central banker respond to this question? Monetary policy has to face a dilemma in dealing with differences in the behaviours among price categories. For example, general price (CPI, PCE, etc.), asset price (productive assets, real estate, land, etc.), commodities price, and equity price, all those four demonstrate different price behaviour and cannot be managed at the same time by conventional monetary policy alone. Here is a statement, which would qualify as a confession, by Masaaki Shirakawa, the ex-governor of the Bank of Japan from April 9, 2008 to March 19, 2013. His statement reveals the paradox of success in the conduct of monetary policy.

"The goal of monetary policy is to achieve sustainable growth with price stability. This is a well-established principle that is shared in Japan, the United Kingdom and globally, regardless of whether an inflation targeting framework is adopted. The more successful the conduct of monetary policy is, however, the more stable prices become and the less volatility is seen in economic activity and financial markets. When the expectation prevails that a stable economic and financial environment will continue for a long period of time, it is likely to encourage leverage and maturity mismatches between the assets and liabilities of financial institutions. The greater the leverage and maturity mismatches are, the more exposed the economy is to a possible unwinding triggered by a given event, so the more fragile it becomes. The bursting of bubbles is the materialization of such fragility. (…) Focusing obsessively on the short-term stability of the consumer price index as a way to ensure economic stability will actually have the opposite effect of increasing instability.” (Shirakawa, 2012, January 10)

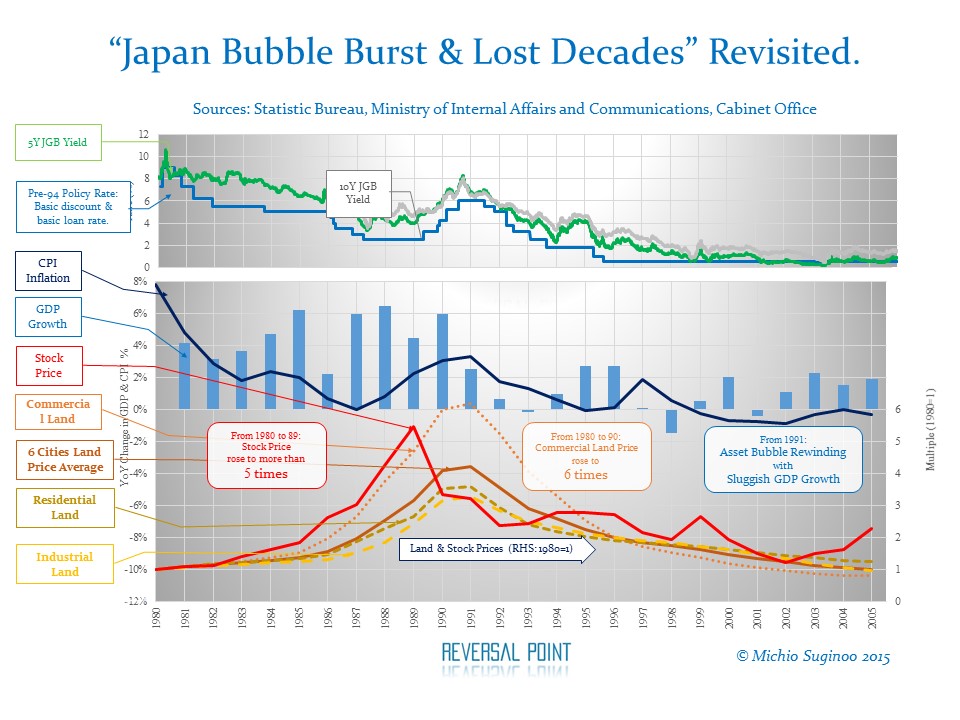

The following chart, covering Japan’s Asset Bubble in the 1980s and the aftermath of its reversal-or its inevitable unwinding-since 1990 to 2007, validates Shirakawa’s paradoxical view.

Monetary policy in the early 1980s resolved the old problem of the 1970s, inflation. In the chart, as the Bank of Japan’s effort in reducing money supply effectively brought down the inflation rate from 8% to 2% by 1983, the policy interest rates followed and declined gradually from 8% to around 6% during the same period to maintain the stability of the economy. As it managed to maintain the economy at positive GDP growth, by gradually lowering interest rate, a side effect emerged throughout the 1980s, a new cycle of finance-fed asset bubble. Declining interest rates, providing easy money to investors, invoked the progressive momentum of asset price rise, both in land and in stock prices: as an example, commercial land inflated to 8 times from 1980 to 1990. The central bank lagged in response by waiting until 1989 to raise the policy rate. At the highly leveraged inflated price level, the monetary policy made its effect immediately on asset prices. Asset price reversed its course to start descending. Accordingly, so did the leveraging momentum. It enters into deleveraging process, or debt-liquidation phase if you like. In contrast to the pace of asset price rise, the deleveraging process caused a prolonged asset deflation and casted a long period of economic stagnation: while asset rise took about 8 to 10 years, asset deflation took multiple decades.

As Irving Fisher (1933) formulated in his “Debt-deflation Theory,” debt-deflation unfolds: a decline in asset price, translating into the deterioration in collateral value, leads to debt-liquidation; debt-liquidation leads to a further decline in asset price; the chain reaction can lead to a deflationary spiral, especially in absence of fiscal intervention. (Fisher, 1933)

Overall, a success in resolving an old problem, inflation reflected in general price proxied by CPI, leads to a new problem, Asset Speculation, then its bubble.

This chart reveals a chain of paradoxical reality, validating what Shirakawa envisioned through his professional monetary management career. Shirakawa, throughout his governance between April 2008 and March 2013, demonstrated his vigilance about the complexity and the limitation of monetary policy with his long-term grand vision. Shirakawa managed to maintain his credible professional independence, by resisting against undue demands from all directions for excessive discretionary actions.

In characterizing the burst of Japan’s asset bubble in 1991 and the Great Depression, Koo stylized a common underlying mechanism in his framework of “Balance-Sheet Recession.” (Koo, 2011) Koo’s characterisation of “the balance sheet recession” accords with Irving Fisher’s “Debt Deflation Theory” and Hyman Minsky’s “Financial Instability Hypothesis.” It goes as follows. When a finance-fed systemic bubble bursts, it leads to a subsequent decline in asset price, without changing the nominal value of liabilities: this impairs the balance sheet, or the net asset, of borrowers. The impaired balance sheet deflects borrowers from finance-fed profit maximization mode to deleveraging mode in their attempt to restore the balance sheet. The systemically impaired balance sheet at macroeconomic level leads to poor credit demand; as a result, it paralyzes the money multiplier function of the modern fractional reserve banking system. As long as the balance sheet at macro level is systemically impaired, the money multiplier remains paralyzed. The time-consuming balance sheet adjustment and the paralyzed money multiplier, both together could reinforce each other to cause severe, prolonged post asset-bubble economic contraction. As long as the money multiplier remains paralyzed, monetary policy is incapacitated to reboot the money supply in the economy. Koo characterized the balance-sheet recession as a borrowers’ problem, but not lenders.’ He acknowledged that monetary policy is effective at the outset of the bubble burst in order to prevent a panic of illiquidity, which is a lender’s problem. However, in order to cope with subsequent economic contraction, he prescribed fiscal expansion to replace inactive private demand in order to reboot the money multiplier mechanism. He justified his prescription by postulating that in the absence of private investment demand the government’s borrowing would not account for crowding out. (Koo, 2011)

[3] The Extended Paradox

Shirakawa encapsulates how a successful monetary policy could lead to a finance-fed systemic bubble as an unintended consequence, then, further to account for its inevitable burst. Furthermore, Koo’s “Balance-Sheet Recession,” in parallel with Irving Fisher’s “Debt-Deflation Theory” and Hyman Minsky’s non-neutral money (“Financial Instability Hypothesis”) could extend the Shirakawa’s Paradox further beyond the scope of the creation of bubble and its burst. The burst of finance-fed systemic bubble leads to an asset deflation; the asset deflation would paralyze the money multiplier mechanism of the modern fractional reserve banking system, which serves the core transmission mechanism of the modern monetary policy; the paralyzed money multiplier mechanism, as a natural consequence, incapacitates the monetary policy itself.

At the end, we arrive to a broader picture of a cycle of systemic paradox: in other words, the self-defeating nature of the monetary policy. As a successful monetary policy, which was made in order to resolve old problems by its design, achieves its own goal, it would be bound to yield another problem that would ultimately impair the core mechanism of the monetary policy itself. In brief, a successful monetary policy defeats itself in the course of its own enterprises.

Repeatedly, monetary policy has to face a dilemma in dealing with differences in the behaviours among price categories. General price (CPI, PCE, etc.), asset price (productive assets, real estate, land, etc.), commodities price, and equity price-all those four demonstrate different price behaviour and cannot be managed at the same time by the conventional monetary policy alone. This paradoxical series of monetary enterprise reveals how monetary policy accounts for systemic risk, by managing to contain cyclical problems. This cycle of systemic paradox is ironically in one part a by-product of a large centralised financial cartel, the central bank.

Reference

Fisher, I. (1933). The Debt-Deflation Theory of Great Depressions. Econometrica, 1(4), 337-357. Retrieved from: http://doi.org/10.2307/1907327

Minsky, H. P. (1995, March). Longer waves in financial relations' financial factors in the more severe depressions II. Journal of Economic Issues, 29(1), 83-96. Retrieved 9 18, 2015, from: http://www.jstor.org/stable/422691

Shirakawa, M. (2012, October 9). Evolution of the Bank of Japan’s policies and operations: looking back on fifty years of history. (Remarks at the introductory program on BOJ policie and operations on the occasion of 2012 annual meetings of the IMF/World Bank Group) Retrieved from: http://www.bis.org/

Shirakawa, M. (2012, January 10). Deleveraging and growth: Is the developed world following Japan's long and winding road? Retrieved from: https://www.boj.or.jp/

Koo, R. C. (2011). The world in balance-sheet recession: causes, cure, and politics. Retrieved from: http://www.paecon.net/PAEReview/issue58/Koo58.pdf

Advance Notification about Disclaimers: Please read the "Terms of Use" & "Privacy Policy" of the site before you submit any comment. Your participation in the comment below is deemed an explicit agreement with "Terms of Use" & "Privacy Policy" of the site.