Article 1-1 Minsky’s Non-Neutral Money: Creation, Destruction, and Evaporation of Money Paradoxical Mechanism of Modern Money

Originally published January 24, 2016 Last edited December 10, 2016 By Michio Suginoo

Hyman Minsky revealed the paradox that the very cause of economic instability is contained within the very architecture of economic stability, encapsulating his view in his emblematic phrase, "stability is destabilising." His view was formed with his emphasis on the analysis of modern money. In brief, money and the real economy interact with each other. Money is, therefore, endogenous and not neutral. This reading revisits some of his views on modern money.

[Non Neutrality of Money]

There is a division among economists about the notion of money. Some economists assume that a change in money supply affects only price level, and does not affect our real economic activities, such as output and employment, in the long term. This is the notion of neutral money. On the other hand, some argue that a change in money supply affects our real economic activities even in the long term. This is the notion of non-neutral money. Modern money is primarily created (destroyed) through two major dynamics: debt creation (repayment) through commercial lending in the private sector; and monetary policy by central banks (McLeay, Radia, & Ryland, 2014, p. 16). This article, primarily focusing on the mechanism of the commercial lending in the private sector, outlines the non-neutrality of money, with reference to Hyman Minsky. The first part of the article, Part A, will illustrate the structure of non-neutral money, and the mechanism behind how modern money is created and destroyed under a fractional reserve banking system. The second part, Part B, will illustrate how modern money manifests its non-neutrality.

[Part A: Structure of Modern Money]

[A-1] Notions of Modern Money

In our contemporary world, we expect money to serve several functions: to be a medium of exchange, unit of account, store of value at minimum, and, in a credit economy world, arguably a standard of deferred payment.

When we look back at the historical evolution of money, in a post barter-trading world, rudimentary money prior to the emergence of promissory notes might have only been in the form of commodity metallic money. In such a case, the identity might be established between money and metallic coins in circulation. During the metallic standard period, however, promissory notes emerged and gradually transformed the definition of money. In our contemporary world, cheques and debit cards can mobilise deposits in bank accounts for transactions, and even credit cards can mobilise unwarranted, uncertain deferred payment for transactions. In the modern world, money can be defined in a pluralistic manner. Narrow money refers to currency in circulation plus liquid deposits. Broad money refers to narrow money plus a wide range of liquid assets. A precise definition differs from one country to another. For now, the important point is to remind ourselves that the notion of money includes deposits as well as notes and coins in circulation, at minimum, in our contemporary world.

[A-2] Minsky’s View: Mechanism of Money Creation & Destruction

Among various views on the topic of the non-neutrality of money, Hyman Minsky elucidated the paradoxical mechanism of modern money. In this presentation, we will glimpse Minsky’s view of the non-neutrality of money.

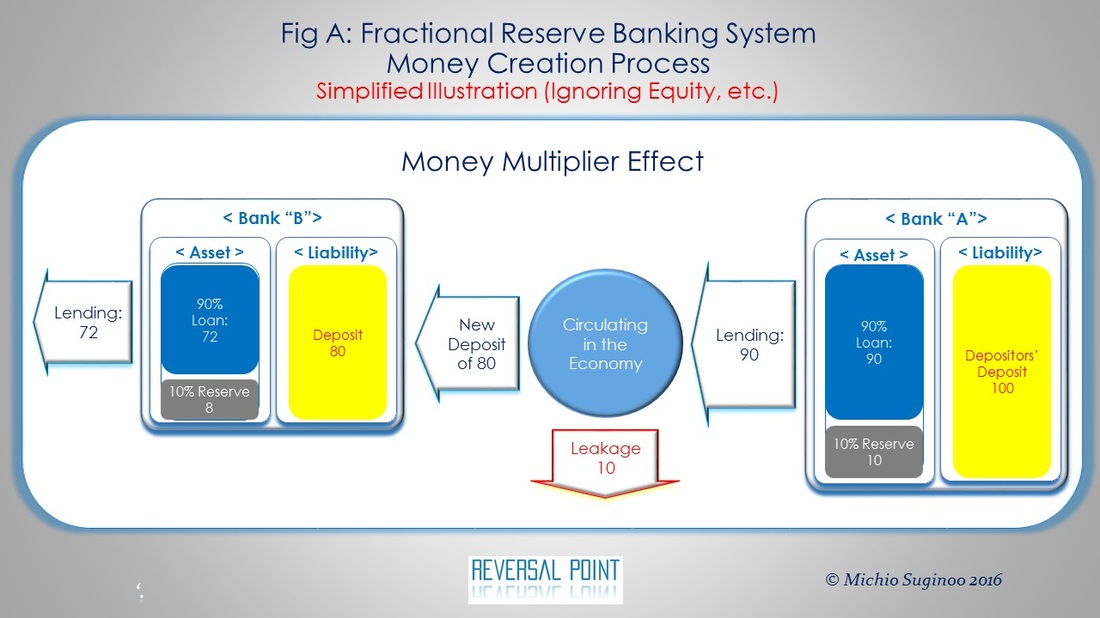

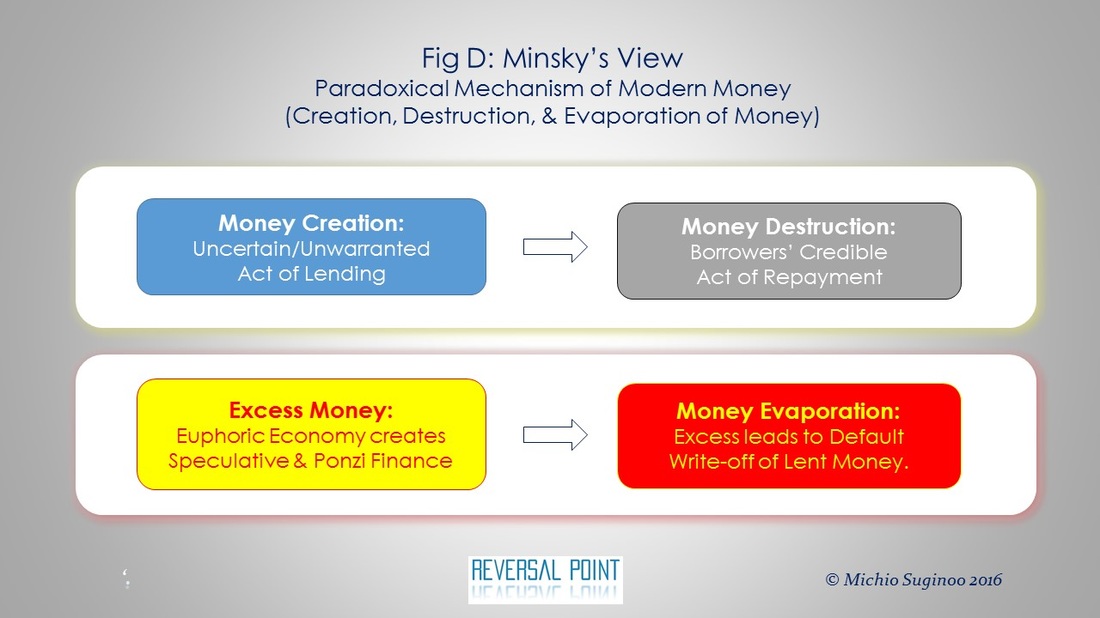

According to Minsky, in the modern capitalist economy, money is not neutral by its design. In Minsky’s words, “bank money arises in financial activity, and the money-creating process includes commitments to make payments that will destroy money.” (Minsky H. P., 1985, p. 13). Repeatedly, modern money is primarily created (destroyed) through two major dynamics: debt creation (repayment) through commercial lending in the private sector; and monetary policy by central banks (McLeay, Radia, & Ryland, 2014, p. 16). Focusing on the private sector's dynamics, Minsky elucidated the mechanism of money creation and its destruction process under the fractional reserve banking system. In addition, in his analysis, Money Multiplier, the ability of the fractional reserve banking system to generate money, is quite variable and not constant at all. (Here is a link for a quick review on Fractional Reserve Banking System and Money Multiplier.)

Simply put, under a fractional reserve banking system, money is created when a bank issues a loan to a borrower, when the borrower’s future repayment ability is uncertain. On the other hand, when the borrower successfully honours the commitment by repaying the loan, money is destroyed in the system. Therefore, the uncertain, unwarranted act of lending leads to “money creation,” while on the other hand, the borrower’s credible act of repayment leads to money destruction. This mechanism is encapsulated in Minsky’s remark: “the creation of money is the first step in a process, in which money is to be destroyed.” (Minsky, 1985, p. 13)

Furthermore, when borrowers default in debt servicing, money evaporates in the system. Of course, although credit risk management is supposed to be designed to mitigate potential negative consequences arising from money evaporation, history of financial crises show that it fails when it is absolutely expected to mitigate or absorb the consequences of default.

In brief, money destruction and evaporation are embedded in the money creation mechanism.

[A-3] Economic Expectations of Actors: Savers, Lenders, & Borrowers

Minsky positioned himself in a philosophical lineage of Keynes’ “General Theory (GT)” where he condemned the neoclassical synthesis of Keynes’ GT in the IS-LM Model (IS and LM refer to the investment/saving curve and liquidity preference/money supply equilibrium curve respectively) and distinguished himself from Keynesian School. Naturally, following GT principles, Minsky viewed that the economic expectations of actors play a significant role in shaping the state of the economy. In addition, according to Minsky, equilibrium at the natural GDP output level might not occur at all. Minsky, loyal to the spirit of Keynes’ GT, conceived that the economy transforms from one disequilibrium to another in general. To Minsky, equilibrium, if any, would be no more than a special ephemeral state. On the contrary, Keynesian's argument hinges on equilibrium, therefore, misrepresents the spirit of Keynes’s GT.

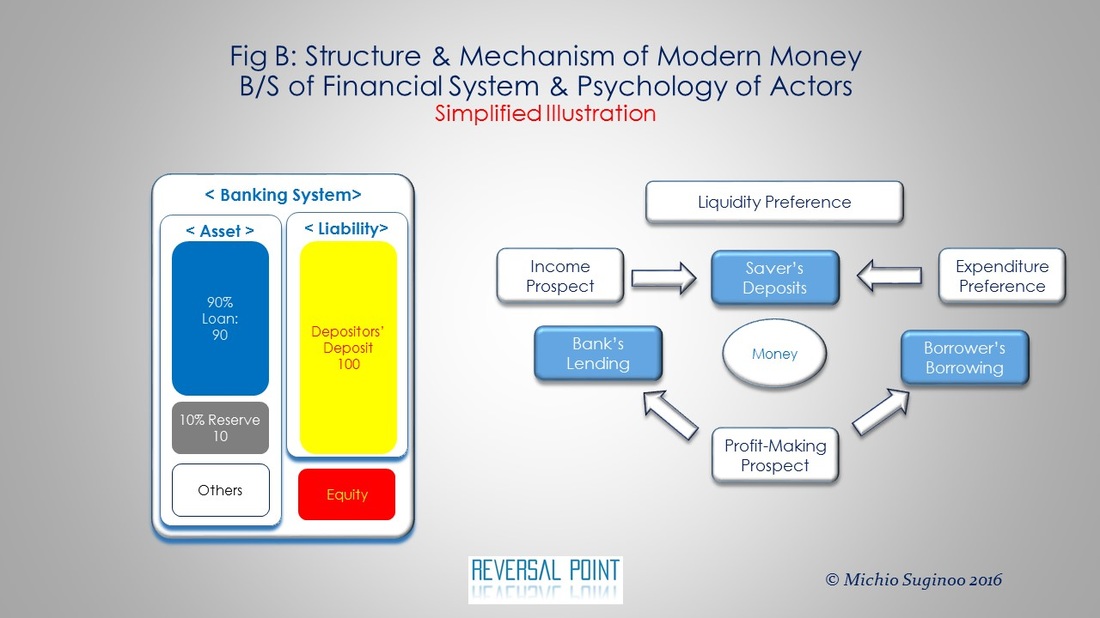

Now, we need to reflect on Minsky’s diagnosis regarding the expectations of the three actors in financing: savers, lenders, and borrowers. When we focus on the commercial lending mechanism, funding originates from deposits of savers. Deposits are affected by trade-offs between the income prospects and expenditure preferences of savers, while lending activities are driven by the “profit expectations” of both borrowers and lenders. Moreover, the liquidity preference of actors can mutate drastically in response to a change in the risk environment. As illustrated later in Part B, a drastic change in liquidity preference would enhance the non-neutrality of money.

(1) Case for Economic Contraction:

Under economic contraction, due to negative profit-making prospects, borrowers’ willingness to borrow recedes. Then, borrowers might even liquidate their existing debts by disposing no-longer profitable assets. Banks, for the exact same reasons, in the middle of rising default prospects, become more restrictive in lending. Savers might prepare for the prospect of a reduction in income and may sacrifice spending to save more. This would increase the supply of funds in the middle of contracting financing demand and reduce interest rates.

If the negative prospect extends beyond cyclical regularity, it might transform the liquidity preference of the actors. If it evokes the prospect of a banking crisis, savers might rush to withdraw their deposits. Consequently, the banking system might suffer from insolvency. In all cases, under economic contraction, the multiplier would most likely decline and create less money.

(2) Case for Economic Expansion:

On the other hand, in an economic expansion, to increase profit-making prospects, borrowers’ willingness to borrow may rise. Banks, in an improving credit condition, may loosen their lending standards to expand profit opportunities. Savers, with better income prospects, might spend rather than save. While deposits may decline and the source of funding for bank lending might shrink, it would unlikely lead to a bank run and may contribute to a slightly higher interest rate. Overall, the engine of money creation can accelerate.

(3) Variable Money Multiplier

The quantity of money generated in commercial lending through a fractional reserve banking system can be gauged by the Money Multiplier, which measures the ability of the fractional reserve banking system to create money. As illustrated above, as the psychology of the three actors transforms the quantity of money creation in the private sector's commercial lending, so does the Money Multiplier. For Minsky, the Money Multiplier increases and decreases according to the psychology of the actors; therefore, it is variable and not constant.

In Minsky’s view, modern money is highly dependent on the financial system’s balance sheet, especially the structure of assets and liabilities of the banking system. Moreover, money creation and destruction interacts with the psychology of three actors: savers, lenders, and borrowers, each with their own profit expectations (income prospects and expenditure preferences) and liquidity preferences. As a result, money is not neutral, but ought to affect real economy. (Minsky H. P., 1985).

Psychological factors constitute the underlying engine of money creation and destruction. Through monetary policy, the central bank can add and reduce fuel into and out of the engine. However, by recalling that Minsky’s non-neutral money theory assumes the variable money multiplier, we can infer that a change in the fuel level by central banks would play only a secondary role depending on the state of the engine. As an example, so long as an engine of a car is active, adding fuel might translate into acceleration. If the engine breaks down, however, fuel has no impact on the system.

Minsky wrote, “This financing relation—in which money is like a bond—is the essential reason why money in our economy is not neutral.” (Minsky H. P., 1985, p. 13)

Up to now, we’ve reviewed the basics of how modern money is structured in private and commercial lending, with an emphasis on Minsky’s view. This section is essential reading for us to understand Minsky's remark, "stability is destabilising," which we will cover next.

[Part B: Manifestation of Non-Neutrality of Money]

For the remainder of this article, this section outlines how modern money could manifest its non-neutrality, summarizing the view found in Minsky’s emblematic phrase, “stability is destabilising,” which he owes to Abba Lerner.

[B-1] Minsky’s Three Classification of Lending

Hedge Financing, Speculative Financing, and Ponzi Financing.

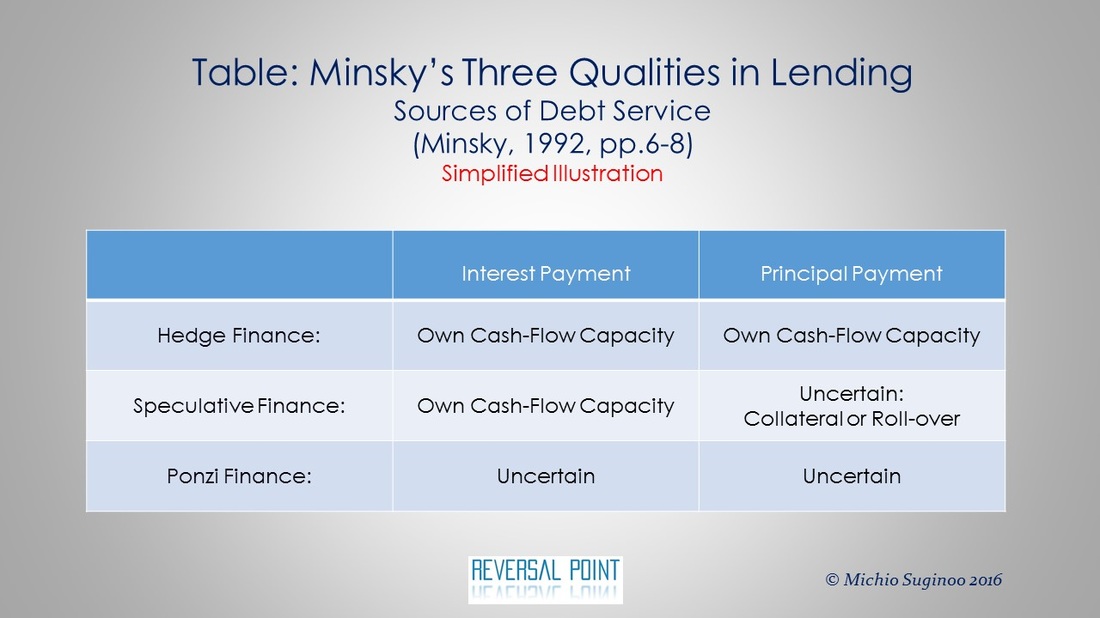

In characterising the transformation in the quality of bank lending, Minsky classified bank lending into three categories, according to a borrower’s debt servicing ability: hedge financing, speculative financing, and Ponzi financing. For the purpose of this presentation we have simplified Minsky’s characterisation of the three types of financing.

First, hedge financing occurs when a borrower possesses a sufficient cash-flow generating capacity for debt service in both interest payment and principal repayment (amortization and cumulative sense for lump sum). Second, speculative financing occurs when a borrower’s cash flow generating capacity is sufficient only for interest payments but not for principal repayment, in which case, the borrower needs to roll-over the financing or dispose of collateral assets in order to commit to principal repayment of the existing debt. Third, Ponzi financing occurs when a borrower possesses neither a sufficient cash flow generating capacity nor a sufficient collateral portfolio for debt service (for both interest payments and principal repayment). In the absence of roll-over, the debt commitment might be partially honoured only by the disposition of the borrower’s asset(s) to the limited extent of its disposition value, if any. Asset liquidation would deteriorate the balance sheet of the borrower and impair the margin of safety for the debt holder—the bank. (Minsky H. P., 1992, pp. 6-8)

[B-2] Stability is Destabilising: Economic Stability, Euphoria, and Bust

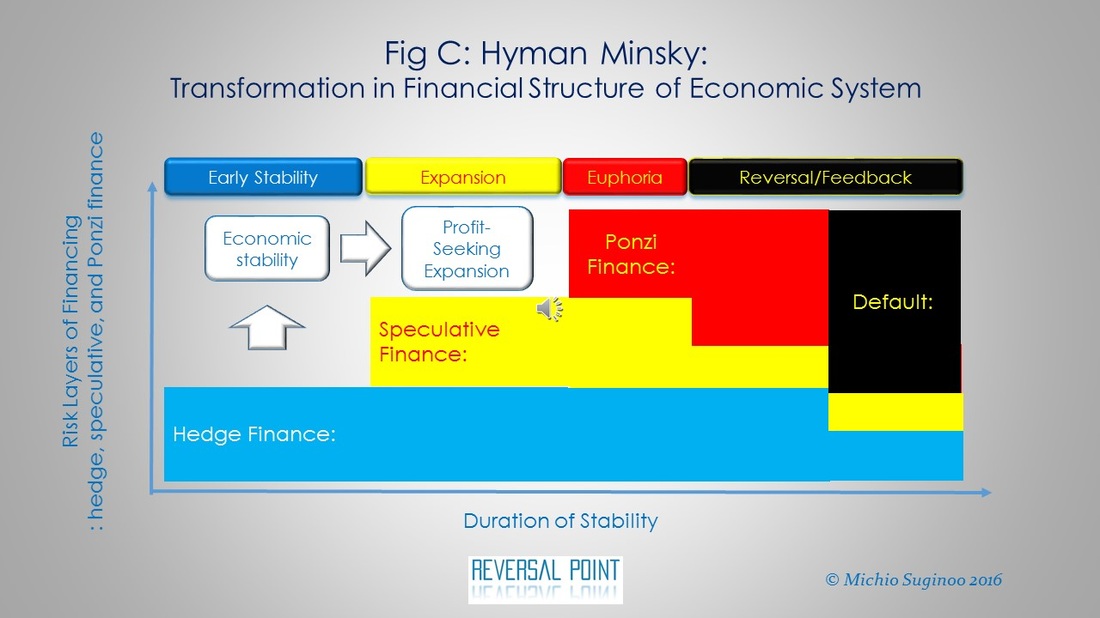

In his explanation of the paradoxical mechanism for how financial stability leads to financial instability, Minsky ascribed it to transformations in the financial structure of the system. In the following section, we will illustrate the transformation along a time horizon.

Figure C illustrates the following summary of Minsky’s exposition on non-neutrality of money: the order flows from the left to the right. On the horizontal axis, we have a time horizon, which represents “duration of stability.” On the vertical axis, we have “the risk layers of financial system” measured by the three classifications of finance: hedge finance, speculative finance, and Ponzi finance. In the early stages of financial stability, the system cannot afford limited “speculative finance” and “Ponzi finance”; therefore, “hedge finance” dominates the system. The dominance of “hedge finance” helps the economy remain self-contained and stabilise itself.

As economic stability gains firmer ground, it improves profit expectations and transforms the psychology of actors. Minsky wrote, “An essential aspect of a euphotic economy is the construction of liability structures which imply payments that are closely articulated directly, or indirectly via layerings, to cash flows due to income production”. (Minsky H., 1970, p. 14)

A rise in profit expectations would stimulate demand for those sources that produce returns, for example, a productive asset from which a higher return is expected to be derived. An expansion of productive capacities would be a time-consuming project— such as construction and renovation—which by nature lags in time in response to the rise in demand. Such inherent inelasticity will cause a net shortage of supply. The net shortage would result in a medium-term rise in value. In a lending context, and with other conditions constant, an increase in the value of net assets would create more room for financing. Moreover, a higher demand for financial resources raises interest rates and pressures lenders to issue new loans at new higher interest rates. (Minsky H., 1970, pp. 7-14)

For the owner of those productive assets, while the value of such assets rises on one hand, the value of the liabilities remains fixed on the other, which, with other factors constant, automatically translates into an improvement in their equity. A better equity valuation and an improvement in risk prospects will make safe assets unattractive and boost riskier assets, such as equity.

Consequently, competition intensifies and the pressure for higher returns builds. Risk-taking mode then sets in. As the protracted period of prosperity creates both pressures and a false sense of the ramifications of higher yields, the profit-seeking activities by those actors—financial intermediaries and borrowers in particular—transform the financial structure by expanding “speculative finance” and “Ponzi finance.” As a result, a euphoric period will feed the very cause of instability: excess money. In this manner, real economy and money could reinforce and interact with each other to drive a euphoric economy. Therefore, money is endogenous and non-neutral.

Excess money makes the economy fragile and destabilising. It is because a supply of excess money (feed-in) inevitably results in its own reversal (feedback) and subsequent evaporation. Excess money makes the entire financial system progressively vulnerable to “debt-deflation,” or severe protracted deleveraging process. (Minsky H., 1970) (Minsky H. P., 1995)

When unfavourable economic conditions unfold—for example, a rise in interest rates or an unexpected medium- to long-term decline in income—some proportion of “speculative finance” transforms to become “Ponzi financing.” Moreover, the built-up layer of Ponzi financing reveals its weakness by failing to roll-over its liabilities and starts a cycle of defaults as a feedback process. A series of defaults on loan commitments would evaporate money created through uncertain unwarranted lending activities. (Minsky H. P., 1992, pp. 7-8)

Either way we look at it, the consequential decline in collateral price would deteriorate the present value of many credit financed collateral and transform some existing finances into speculative and Ponzi finances.

[B-3] Evaporation of Money

Now, we will see an illustration of how money evaporates in response to the collapse of asset values. For our illustration, this section will outlines the evaporation of money, focusing on speculative finance. By definition, speculative finance occurs when a borrower’s cash flow generating capacity is sufficient only for interest payments but not for principal repayment, in which case, the borrower needs to roll-over the financing or dispose of collateral assets in order to commit to principal repayment for the existing debt.

After a decline in its asset value, it could further become short of collateral value for debt service. Therefore, an asset decline could downgrade a “speculative finance” into a “Ponzi finance.” Due to the shortage of the financial resource for debt service, it would most likely fail to roll-over the existing debt. Once it fails to roll-over the debt, it has to liquidate its collateral assets at a depressed price. Any shortage in the principal repayment represents the money that was not only destroyed, but also evaporated, because it would not be recovered on the lender’s side. Instead, it is registered as a write-off. Therefore, money can be not only created and destroyed, but also evaporated in the system.

After a protracted period of asset inflation, the asset price can collapse on a broad scale and could unveil the vulnerability of modern money. The symptom is the evaporation of money resulting from defaults from speculative and Ponzi financing. The failure of debt service in those excess lending transactions would trigger a series of asset dispositions. This creates a series of fire sales in an environment where there is limited demand due to dire economic prospects. It would lead to a systemic collapse in asset prices and a large-scale evaporation of money. The financial system then enters into a deleveraging cycle. This accords with Irving Fisher’s “Debt Deflation Theory” (Fisher, 1933).

The real cause other than the shock that might trigger the decline in asset price is rooted in the overextended credits owing to speculative and Ponzi finance during the period of euphoric economy. If there were no asset inflation, asset price collapse might not occur with an emergence of economic shocks [1]. Shocks can emerge from anywhere and their occurrence depends on distinctive factors in each case.

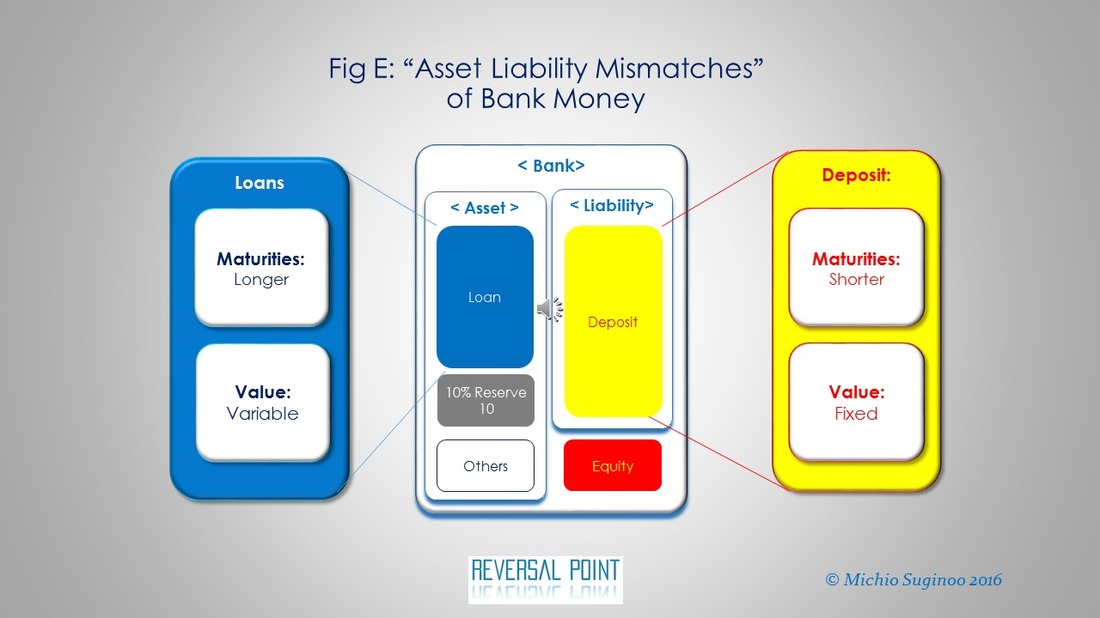

[B-4] Vulnerability of Modern Money: Banking System’s Asset Liability Mismatches

A systemic evaporation of money further unveils a very fundamental vulnerability of the fractional reserve banking system: a bank run [2].

This vulnerability is derived from particular characteristics of the balance sheet within the banking system that modern money depends on. When we compare the assets and liabilities of the banking system, there is a clear set of mismatches. Banks carry deposits on the liability side and loans on the asset side. While this is simplifying the matter somewhat, from a maturity perspective, in principle, the maturities of deposits are shorter than those of loans. From a value characteristic perspective, while nominal values of deposits are fixed, those of loans could be variable when we take defaults into account. Overall, the banking system’s balance sheet has longer-term, variable commitments on the asset side and shorter-term, fixed obligations on the liability side. The mismatches between asset and liability would exacerbate the consequences of a systemic asset deflation.

On the asset side of the banking system, the nominal value of loans is variable, especially according to credit conditions, when we take defaults into account. The maturities of loans are mixed from short to long term and determined at the time of contract (though they may be adjustable afterwards).

On the liability side, from a value perspective, the nominal principal value of deposits is fixed. Deposits consist of demand and time liabilities. In particular, current deposits are demand liabilities, as banks are required to return current deposits to savers on demand. Therefore, actual maturities of current deposits can transform according to the liquidity preferences of savers. Their liquidity preferences can mutate drastically according to the state of the economy. Overall, in relative terms, deposits can be characterised as short-term, fixed obligations.

Those mismatches make the banking system vulnerable to debt-deflation. With its liability fixed in nominal terms, a drastic decline in its asset values would expose the banking system to insolvency beyond illiquidity. Insolvency is more severe than illiquidity, partly because the central bank would have limited, or even no, capacity to resolve it. This illustrates the very reason why a systemic collapse of assets’ values exposes the banking system to a bank run.

A bank run would deprive the banking system of funding. Automatically, the Money Multiplier would collapse and drastically deplete money in the system.

Repeatedly, modern money depends heavily on the balance sheet of the banking system. Those asset-liability mismatches in the banking system—in maturities and nominal value characteristics—enhance the non-neutrality of bank money.

[Summary]

In summary, Minsky revealed the paradox that the very cause of instability is contained within the very architecture of stability.

For Minsky, the balance sheet of financial intermediaries, especially banks, and the economic expectations of actors—savers, lenders and borrowers—play a significant role in accounting for the creation, destruction, and even evaporation of money. Moreover, those transformations in money make the money multiplier variable and affect the state of the real economy. In brief, money and the real economy interact with each other. Therefore, money is endogenous and not neutral.

This article, primarily focusing on commercial lending in the private sector, briefly outlined some aspects of Minsky’s views on the non-neutrality of money, with some modifications and simplifications for illustrative purposes.

Notes:

[1] This does not exclude the possibility of asset price decline in the absence of a preceding asset bubble. Without any asset bubble, there might be other causes to account for a systemic asset price collapse, such as drastic demographic changes. The statement is not a general statement, but context=specific in order to characterise the bubble bust case in our discussion.

[2] Bank runs must have become a common phenomenon with the emergence of promissory notes. Bank runs were common during the gold standard era as well. They are a phenomenon of bank money.

Reference

Fisher, I. (1933). The Debt-Deflation Theory of Great Depressions. Econometrica, 1(4), 337-357. Retrieved from: http://doi.org/10.2307/1907327

McLeay, M., Radia, A., & Ryland, T. (2014). Money creation in the modern economy. Quarterly Bulletin, 4-27.

Minsky, H. P. (1970). Financial instability revisited: the economics of disaster. The Steering Committee for the Fundamental Reappraisal of the Discount Mechanism, The Board of Governors of the Federal Reserve System. Retrieved 9 30, 2015, from: https://fraser.stlouisfed.org/

Minsky, H. P. (1986, 6). The Evolution of Financial Institutions and the Performance of the Economy. Journal of Economic Issues, 20(2), 345–353. Retrieved 9 18, 2015, from http://www.jstor.org/stable/4225715

Minsky, H. P. (1992, May). The Financial Instability Hypothesis. The Levy Economics Institute.

Minsky, H. P. (1995, March). Longer waves in financial relations' financial factors in the more severe depressions II. Journal of Economic Issues, 29(1), 83-96. Retrieved 9 18, 2015, from: http://www..org/stable/422691