Intellects in antiquity, Socrates, Plato and Polybius, diagnosed terminal symptoms of democracy: democracy is doomed to degenerate into either tyranny or ochlocracy (mob rule); and the rise of demagogues is an omen for the paradigm shift.

Does this notion, especially rise of demagogues, cast a parallel to our contemporary political reality? Is our contemporary reality experiencing a recurrence of Zeitgeist (the spirit of epoch) in our own context? If our reality is a by-product of three forces—recurrence, evolution, and endogenous dynamic—can we EVOLVE out of a vicious cycle? This series, ‘Zeitgeist, Zero Hour,’ is a partial summary preview, or ‘synopsis’ if you like, of my forthcoming ‘self-publishing’ project. To view its first content, please click: "Zeitgeist, Zero Hour: Return of Tyranny. Zeitgeist Zero Hour:

|

|

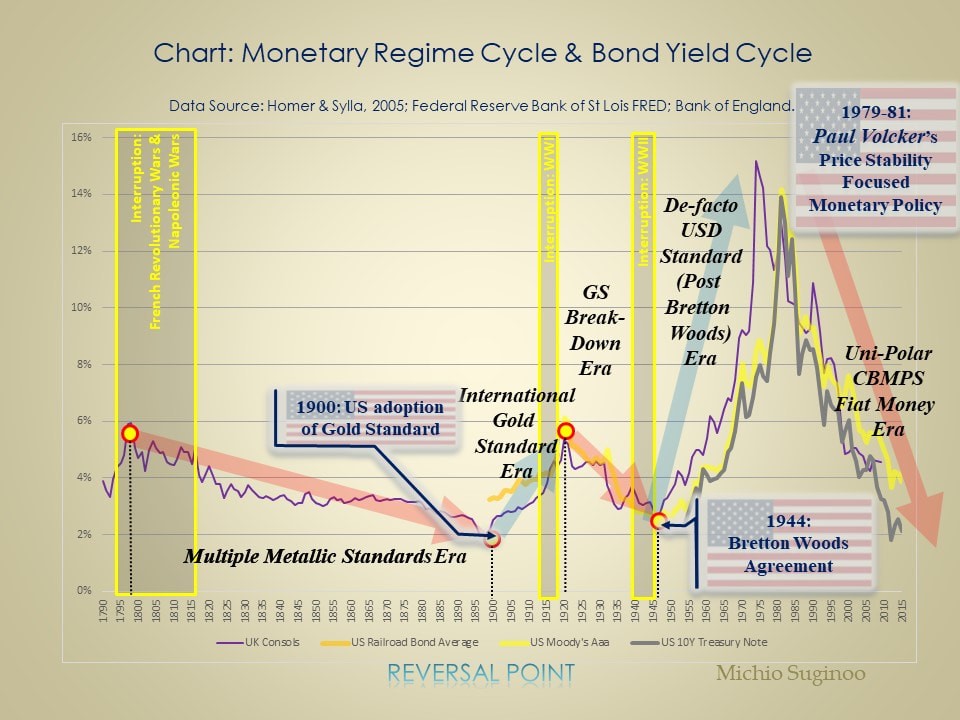

Sidney Homer (1902–1983), one of the most distinguished, innovative bond investment experts of his time, discussed the hypothetical relationship between the cost of financing and the development of ancient western civilizations. And Homer illustrated his notion by projecting in a chart the centennial minimum interest rate floor (let us call this concept the “lowest interest rate frontier”) throughout three ancient civilizations: Babylonian, Greek, and Roman. His chart of the lowest interest rate frontier demonstrated the presence of a common supra-secular rhythm among all three civilizations.

Homer’s implication is that the state of money, when expressed in the supra-secular cycle of interest rates, might reveal stages of the western civilization cycle. Homer extended his analogy to the Post–Dark Age Western world. We can draw inferences relevant to our own time using Homer's analogy. |

|

This series explores the notion that the state of money, when expressed in interest rate cycle, mirrors the state of social, political, and economic reality.

Bond wave demonstrates a complex rhythm that expresses both indisputable uncertain irregularities and equally undeniable pendulum-like recurrent dynamics. This section overviews those features and builds the foundation for bond wave mapping, which is illustrated in the following case studies―Regime Change in International Monetary System, Price Cycle, Private Debt Cycle, Fiscal Cycle. |

The Bond Wave Mapping

To capture recurrences and evolutions in the secular rhythm of the bond wave, I devised a simple technique called “bond wave mapping.” This technique captures the interactions of secular rhythms between the bond wave and other metrics. This simple method—primarily using crude data—enables us to extract hidden information about the bond wave as historical facts, loosening the confines of economic doctrines.

In brief, the bond wave is a manifestation of socio-economic and political realities. Bond wave mapping provides a heuristic way to apply historical analogy to make inferences about our present and future based on our past.

The following contents are sample exercises showing the use of bond wave mapping to extract the hidden implications of this complex secular rhythm.

In brief, the bond wave is a manifestation of socio-economic and political realities. Bond wave mapping provides a heuristic way to apply historical analogy to make inferences about our present and future based on our past.

The following contents are sample exercises showing the use of bond wave mapping to extract the hidden implications of this complex secular rhythm.

|

|

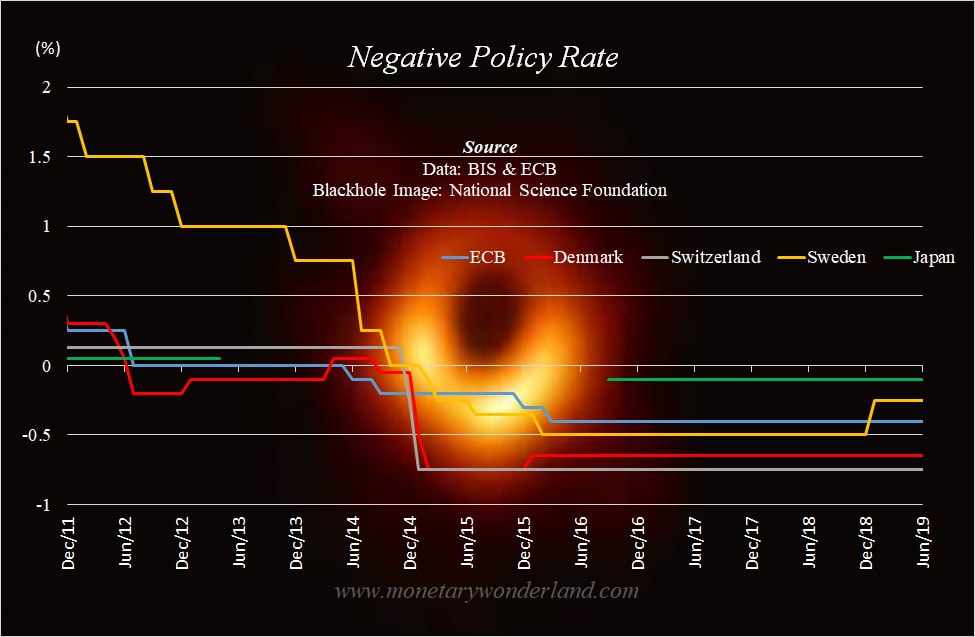

Looking back, the paradigm transformations in currency regimes, or international monetary systems, show patterns along the bond wave. The past five bond waves have mirrored the tendencies of the rhythm in international monetary arrangements to manifest milestone events in regime transformations at both extreme ranges—top and bottom—of the bond wave. As of this writing, given our position within the bottom range of the bond wave (in terms of bond yield levels), we are compelled to ask a legitimate question about whether we may be entering a new paradigm in the international monetary system.

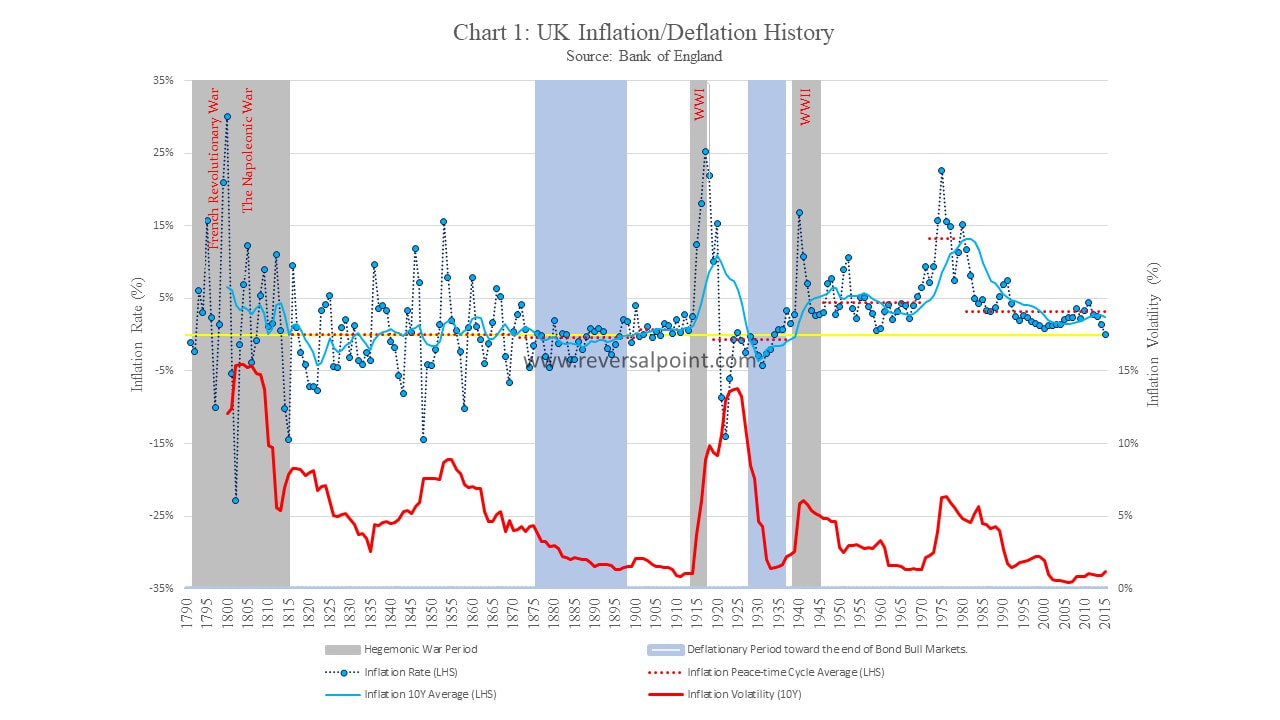

In the past, the bond yield’s behaviour relative to price behaviour demonstrated two fundamentally distinct paradoxes: Gibson’s Paradox (for more than two centuries between the 18th century and the 1970s) and Shiller’s Paradox (since the 1980s). The shift in the paradoxical nature of the bond wave confirms the historical fact that an established relationship between behaviours of the bond yields and price can break down. Along with this relationship, war cycles also demonstrated a shift in their established relationship with price behaviour (the inflation cycle). In addition, along the bond wave, the behaviour of deflation changed as the paradigm shifts in the currency regime took place.This content examines these transformations in the relationship between the bond wave and price behaviour. About the prospect of the relationship, what can we learn from the past? (click: Price and Inflation Cycles along the Bond Wave)

The bond wave located two systemic financial crises—the Great Depression and the Global Financial Crisis—in analogous bond wave locations (in the middle of the two bull waves: the Vacuum Wave [1920-46] and the Globalization Wave [1982-ongoing as of September 2016]) and demonstrated a remarkable synchronization with the private debt-cycle. Along the bond wave, we explore similarities and differences in the behaviours of private debt cycles for these two systemic financial crises.

In addition, this case study revisits the mechanisms of systemic financial crisis addressed by three economists: Irving Fisher, Hyman Minsky, and Richard Koo. (Click: The Private Debt Cycle along the Bond Wave) The primary purpose of sovereign debt has changed from war finance to fiscal expansion in the past. Along with this transformation, the emergence of massive sovereign debt issuance shifted from the top range to the bottom range of the bond wave.

Before that, WWI, a hegemonic war, tended to coincide with inflationary environments. This inevitably caused a notable surge in sovereign debt at the top range of the bond wave. In modern times, a massive fiscal expansion tends to emerge in the aftermath of a systemic financial crisis, in other words, during a deflationary environment. This inevitably triggers a drastic surge in sovereign debt at the bottom range of the bond wave. Moreover, some governments deploy “inflating away,” a technical default, in the context of sovereign debt management. These dynamics―war cycles, private debt cycles, sovereign debt cycles, and “Inflating Away” ―were interrelated and demonstrated some patterns in the rhythms in the behaviour of massive government interventions in the past. This content, with bond wave mapping, attempts to make inferences about what the past might illuminate about the prospects for massive- scale government interventions. (click: Government Intervention Cycles along the Bond Wave) "Bond Wave Mapping": Case Study X

Political Cycle along the Bond Wave Under Construction |

|

Michio Suginoo, CFA® (Chartered Financial Analyst)

Founder of www.reversalpoint.com

Owner of www.monetarywonderland.com

Founder of www.reversalpoint.com

Owner of www.monetarywonderland.com

This website is operated independently by Michio Suginoo. Your contibutions to support this web site are welcome. For your contributions, please visit "Your Support."

Copyright © 2015-2019 by Michio Suginoo. All rights reserved.