|

BOND WAVE MAPPING: CASE STUDY 1 Paradigm Transformations in International Monetary System Along the Bond Wave Originally published July 23, 2016

Last edited December 2, 2021 by Michio Suginoo Sidney Homer, projecting the centennial best credit frontier (the lowest interest rate in each century), left us a notion that the state of money has something to do with the evolution of the Western civilization. Homer’s notion extends to a life cycle of civilization: there are some relationship between the supra-secular cycle of interest rates and the civilization cycle.

Inspired by this notion presented by Sydney Homer, I intend to contemplate the cyclical relationship between the interest rates and our political economic reality in a shorter horizon, say secular time frame. In other words, using the bond wave—by observing a long-term transformation in the relationship between bond yields and other metrics for an extended period of time—my attempt is to capture a notion that the state of money mirrors a broader socio, political, and economic reality. Bond wave mapping provides a heuristic approach to apply historical analogy to make inferences about our present and future based on our past. In this attempt, we assume that our reality is driven by three forces at least: cyclical force, evolutionary force, and accidents (uncertainty). This section reviews the transformation in currency regime along the bond wave.

|

|

1) Multiple Metallic Standards Era:

Throughout the Victorian Wave, the international monetary arrangement was plural. During the early stage of this wave, multiple international monetary systems existed across major economies: the United Kingdom was the only gold standard state; the German speaking states were under the silver standard; others, including France, were under the bimetallic standard. Since 1871, with the Unified German Empire’s adoption of the gold standard, advanced economies have gradually gravitated toward the gold standard. (Eichengreen, 2008, p. 9) The US adoption of the gold standard in 1900, at the bottom of the International Gold Standard Wave, completed the convergence among major contemporary economies. 2) International Gold Standard Era: Thereafter, throughout UK peace time during the International Gold Standard Wave, the international monetary arrangement became relatively singular, gold standard, among advanced economies until WWI broke this trend. 3) Gold Standard Break-down Era: Chart 3.1.1 reveals that in 1919, within the top range of the International Gold Standard Wave, the peace-time GBP/USD exchange rate collapsed for the first time since its 19th century post-war recovery in 1821 from the aftermath of the Napoleonic War. Although the Bank of England managed to defend gold convertibility by devaluing its currency during peace time, it significantly compromised its conduct of the gold bullion standard. In hindsight, this peace-time compromise marked an auspice of collapse in the gold standard system. Although the United Kingdom managed to maintain its convertibility, it also compromised its conversion rate. Finally, in 1931, the Bank of England announced the first peace-time suspension of gold convertibility. Hereafter, through the “Vacuum Wave” until the adoption of the Bretton Woods System, the GBP collapsed against the USD. In brief, the “Vacuum Wave” invalidated the gold standard as an operating currency regime of the time. Post-WWI period manifests the break-down of the gold standard. 4) USD Standard Era: In the aftermath of WWII, the Bretton Woods System was designed as a variant of the gold-exchange standard, which allowed central banks to substitute foreign exchange reserves for gold reserves. By its statute, the Bretton Woods System did not prohibit the gold convertibility of non-USD currencies. Nevertheless, it transformed to a de-facto gold-USD standard because of economics as the rest of the world demanded USD as gold-reserve substitutes because of the US’s predominant economic position. Within the top range of the Reconstruction Wave, a series of events that undermines the Post Bretton Woods USD standard emerged.

5) Uni-Polar Fiat Money Central Banker’s Monetary Policy Standard: Volcker's move during 1979-1981 was a strong political announcement that the new monetary regime, fiat money, needs to be managed by central bankers with a special attention to price stability. In other words, the new monetary regime is not merely fiat money, but also "Central Banker's Monetary Policy Standard (CBMPS)." Thereafter, throughout the Globalization Wave, among major advanced economies fiat money has become operated in a floating exchange rate system with price stability foduced monetary policy managed by central bankers. It was also characterised by the dominance of USD as the global reserve currency: in other words, “Uni-Polar Fiat Money CBMPS System” under USD dominance. During this bull wave, the EURO—the European monetary union in the absence of fiscal union—emerged to compete with the USD in search of better seigniorage. Despite such new developments, the USD demonstrated its superiority in the aftermath of the global financial crisis. |

Revision Announcement (2 December, 2021)

The original description regarding the Bretton Woods System in the section of 4) USD Standard Era was misleading. Thus, the following revision was made.

Michio Suginoo, 2 December, 2021

- Original Statement: At the end of WWII (at the bottom of the bond yield cycle) the Bretton Woods System introduced a de-facto US Dollar Standard in disguise of a pseudo-Gold Standard, in which USD was the only currency convertible to gold and the rest of currencies were loosely pegged to USD. This arrangement significantly compromised the metallic convertibility of currency and marked the first step toward fiat money regime.

- Revised Statement: “In the aftermath of WWII, the Bretton Woods System was designed as a variant of the gold-exchange standard, which allowed central banks to substitute foreign exchange reserves for gold reserves. By its statute, the Bretton Woods System did not prohibit the gold convertibility of non-USD currencies. Nevertheless, it transformed to a de-facto gold-USD standard because of economics as the rest of the world demanded USD as gold-reserve substitutes because of the US’s predominant economic position."

Michio Suginoo, 2 December, 2021

These developments marked the gradual footsteps of the paradigm shift of international monetary arrangements from one extreme to another—from a fixed exchange rate regime under a metallic standard to a floating exchange rate regime under fiat money managed by central banker’s price stability focused monetary policy. And the timeline in the transformations of international monetary regime demonstrated a remarkable synchronization with the passage through the past 5 bond waves.

Our current position is near at the bottom of the bond wave, suggesting an extreme monetary condition. If history is a guide, this low range of the bond wave suggests that a new paradigm transformation could unfold in the international monetary system.

If that is the case, what sort of transformations should we expect? Will such change be sudden? Or will there be a gradual change over the next few bond waves? Will there be some sort of extension of our current regime, or will we encounter a totally new regime that the world has never experienced before? If history is a guide, in order to gain some insights into these questions, it is worthwhile revisiting historical transformations of the international monetary regime.

Our current position is near at the bottom of the bond wave, suggesting an extreme monetary condition. If history is a guide, this low range of the bond wave suggests that a new paradigm transformation could unfold in the international monetary system.

If that is the case, what sort of transformations should we expect? Will such change be sudden? Or will there be a gradual change over the next few bond waves? Will there be some sort of extension of our current regime, or will we encounter a totally new regime that the world has never experienced before? If history is a guide, in order to gain some insights into these questions, it is worthwhile revisiting historical transformations of the international monetary regime.

Bond Wave Mapping with Currency Exchange Rate

Below, we will demonstrate how these observations are located by “bond wave mapping.” The technique is simple. In order to capture the timeline of transformations in the international monetary regime, we project two monetary metrics—the currency exchange rate and the monetary authority’s gold stock—on the bond wave.

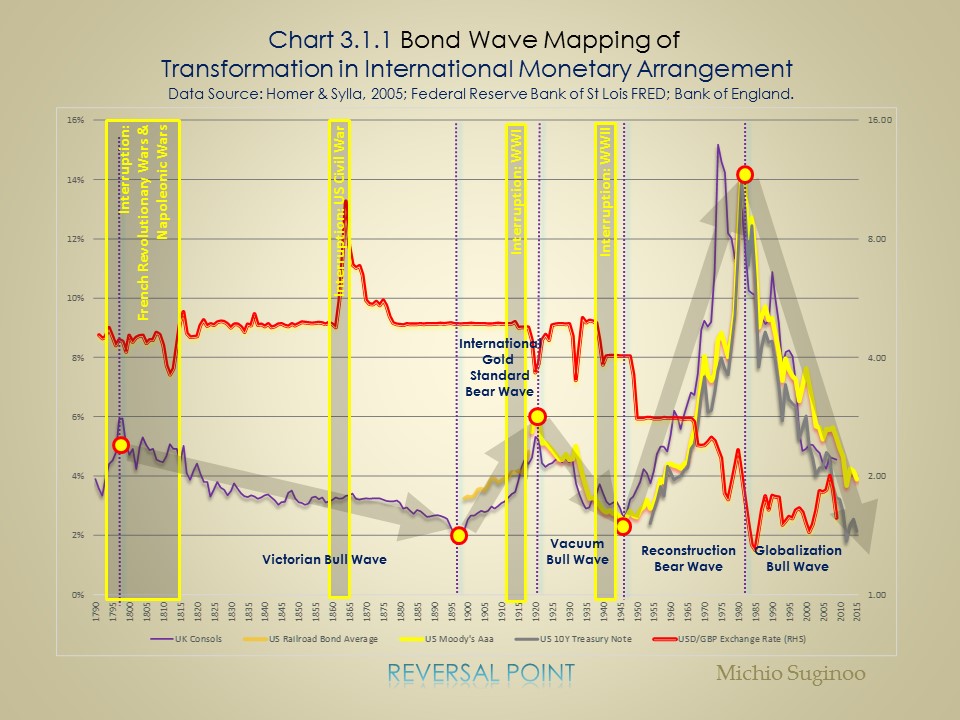

First, we start with the bond wave mapping using the currency exchange rate in Chart 3.1.1.

First, we start with the bond wave mapping using the currency exchange rate in Chart 3.1.1.

Before WWI, the most salient feature in the currency exchange rate is two large swings. In principle, both the United Kingdom and the United States were conducting fixed currency exchange rates during peace time under the metallic standards―the gold standard for the United Kingdom and the bimetallic standard for the United States. These swings were due to extraordinary contingencies. As a matter of fact, the exchange rate is quite flat for the rest of the period prior to WWI. This flatness represents the ordinary state of currency regime, fixed rate, of the epoch prior to WWI.

The first large swing was downward, and represented the devaluation of the GBP vs USD: it was due to the UK’s contingency suspension of its gold convertibility in order to cope with the extraordinary economic and political circumstances surrounding the French Revolution and the Napoleonic Wars. The second large swing was upward, and represents the devaluation of the USD vs GBP: it was due to the United States’ contingency suspension of metallic convertibility for the Civil War. Repeatedly, except for those swings, the exchange rate between these two currencies was relatively flat and demonstrated the nature of fixed exchange rate conduct under a metallic standard regime.

Metallic convertibility was the cornerstone of the metallic standard during ordinary peace time. (Eichengreen, 2008, p. 9) However, during extraordinary contingencies, such as wars, the metallic standard allowed the state to suspend its convertibility on the condition that it would resume it once ordinary economic conditions were restored. In this sense, these two large swings accord with the temporary contingency rule built within the metallic standard. In other words, each of these two large deviations was temporary, and did not constitute the abolishment of the metallic standard.

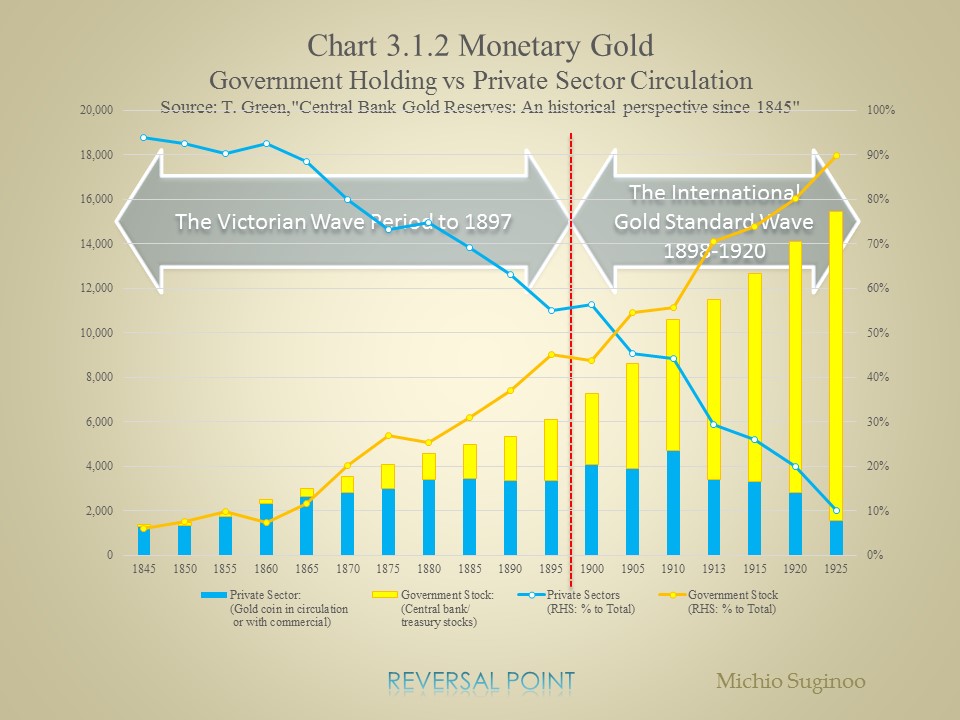

During the same period, a gradual transformation took place in the international monetary arrangement toward the end of the Victorian Wave: the currency regime among advanced economies was gradually consolidated into the gold standard. At the turn of the 20th century, when the International Gold Standard Wave commences, major advanced economies were all operating gold standard. The transition between these two waves is captured by a bond wave mapping using the government gold stock (Chart 3.1.2).

Moving forward, the Vacuum Wave already demonstrates the gradual collapse of the conventional UK centric gold standard. Coming into the Vacuum Wave, Chart 3.1.1 shows the first peace-time breach of the fixed exchange rate in GBP devaluation in a century—since its post-war restoration of the fixed exchange in 1821 in the aftermath of the Napoleonic Wars. Peace-time compromise of the fixed exchange rate was rarely seen in the ordinary conduct of the UK gold standard in the past. Although the Bank of England defended its gold convertibility by devaluing its currency, it started compromising the convertible rate. The gold price at £3.17s. 10d. per troy ounce, originally set by Isaac Newton in 1717, lasted for about two centuries but finally came to collapse. On the other hand, the USD maintained its conventional convertible rate. This contrast reflects the shift in the centre of economic power from the United Kingdom to the United States. (Green, 1999, p. 11)

Against the backdrop of these developments, Peter Bernstein (2000) reminds us in The Power of Gold of the caveat offered by former prime minister Benjamin Disraeli:“It is the greatest delusion in the world to attribute the commercial preponderance and prosperity of England to our having a gold standard. Our gold standard is not the cause, but the consequence of our commercial prosperity.” (Bernstein, 2000, p. 258)

Within the top range of the Vacuum Wave, the symptom surfaced in the first peace-time GBP devaluation and marked the beginning of the collapse of the UK gold standard. Despite Disraeli’s caveat, the Bank of England made an abortive attempt to restore gold conversion at pre-WWI parity in 1925. This move was proven to be a historic mistake. As the chart illustrates, although the GBP managed to recover versus the USD for a short period of time, after the end of WWII it failed to return to pre-war parity and collapsed against the USD for good.

At the near bottom of the Vacuum Wave, among major contemporary economies, the new international monetary arrangement, the Bretton Woods System, was instituted one year before the end of WWII: it operated during most of the Reconstruction Wave. The new system was a de facto USD standard in which only the USD was convertible with gold bullion and all other currencies were pegged to the USD. The adjustable peg allowed a state to reduce its balance-of-payment deficits technically, and capital controls were allowed to limit the international capital flow. (Eichengreen, 2008, p. 91)

As the currency exchange rate chart suggests, this arrangement helped maintain the fixed rate between these two currencies in the early stage, but failed to do so later, even before Nixon’s announcement that the US would abolish gold convertibility. This was the consequence of market forces denouncing the system. The new system lost the ability to maintain the fixed exchange regime as its ordinary peace-time conduct. As a result, the floating exchange rate regime emerged within the top range of the Reconstruction Wave.

Since then, throughout the Globalization Wave, the floating exchange rate under fiat money regime has dominated most advanced economies’ ordinary conduct in the international monetary system.

Chart 3.1.2 shows the proportions of monetary gold held by governments versus in private circulation. With this chart, we will confirm the paradigm transformation in the international monetary arrangement at the turn of the 20th century. This chart only covers the period 1845 to 1925, illustrating an overview of the transformation that took place between the Victorian Wave and the International Gold Standard Wave. Since this chart omits the bond wave chart, it accompanies signs to identify those periods.

The first large swing was downward, and represented the devaluation of the GBP vs USD: it was due to the UK’s contingency suspension of its gold convertibility in order to cope with the extraordinary economic and political circumstances surrounding the French Revolution and the Napoleonic Wars. The second large swing was upward, and represents the devaluation of the USD vs GBP: it was due to the United States’ contingency suspension of metallic convertibility for the Civil War. Repeatedly, except for those swings, the exchange rate between these two currencies was relatively flat and demonstrated the nature of fixed exchange rate conduct under a metallic standard regime.

Metallic convertibility was the cornerstone of the metallic standard during ordinary peace time. (Eichengreen, 2008, p. 9) However, during extraordinary contingencies, such as wars, the metallic standard allowed the state to suspend its convertibility on the condition that it would resume it once ordinary economic conditions were restored. In this sense, these two large swings accord with the temporary contingency rule built within the metallic standard. In other words, each of these two large deviations was temporary, and did not constitute the abolishment of the metallic standard.

During the same period, a gradual transformation took place in the international monetary arrangement toward the end of the Victorian Wave: the currency regime among advanced economies was gradually consolidated into the gold standard. At the turn of the 20th century, when the International Gold Standard Wave commences, major advanced economies were all operating gold standard. The transition between these two waves is captured by a bond wave mapping using the government gold stock (Chart 3.1.2).

Moving forward, the Vacuum Wave already demonstrates the gradual collapse of the conventional UK centric gold standard. Coming into the Vacuum Wave, Chart 3.1.1 shows the first peace-time breach of the fixed exchange rate in GBP devaluation in a century—since its post-war restoration of the fixed exchange in 1821 in the aftermath of the Napoleonic Wars. Peace-time compromise of the fixed exchange rate was rarely seen in the ordinary conduct of the UK gold standard in the past. Although the Bank of England defended its gold convertibility by devaluing its currency, it started compromising the convertible rate. The gold price at £3.17s. 10d. per troy ounce, originally set by Isaac Newton in 1717, lasted for about two centuries but finally came to collapse. On the other hand, the USD maintained its conventional convertible rate. This contrast reflects the shift in the centre of economic power from the United Kingdom to the United States. (Green, 1999, p. 11)

Against the backdrop of these developments, Peter Bernstein (2000) reminds us in The Power of Gold of the caveat offered by former prime minister Benjamin Disraeli:“It is the greatest delusion in the world to attribute the commercial preponderance and prosperity of England to our having a gold standard. Our gold standard is not the cause, but the consequence of our commercial prosperity.” (Bernstein, 2000, p. 258)

Within the top range of the Vacuum Wave, the symptom surfaced in the first peace-time GBP devaluation and marked the beginning of the collapse of the UK gold standard. Despite Disraeli’s caveat, the Bank of England made an abortive attempt to restore gold conversion at pre-WWI parity in 1925. This move was proven to be a historic mistake. As the chart illustrates, although the GBP managed to recover versus the USD for a short period of time, after the end of WWII it failed to return to pre-war parity and collapsed against the USD for good.

At the near bottom of the Vacuum Wave, among major contemporary economies, the new international monetary arrangement, the Bretton Woods System, was instituted one year before the end of WWII: it operated during most of the Reconstruction Wave. The new system was a de facto USD standard in which only the USD was convertible with gold bullion and all other currencies were pegged to the USD. The adjustable peg allowed a state to reduce its balance-of-payment deficits technically, and capital controls were allowed to limit the international capital flow. (Eichengreen, 2008, p. 91)

As the currency exchange rate chart suggests, this arrangement helped maintain the fixed rate between these two currencies in the early stage, but failed to do so later, even before Nixon’s announcement that the US would abolish gold convertibility. This was the consequence of market forces denouncing the system. The new system lost the ability to maintain the fixed exchange regime as its ordinary peace-time conduct. As a result, the floating exchange rate regime emerged within the top range of the Reconstruction Wave.

Since then, throughout the Globalization Wave, the floating exchange rate under fiat money regime has dominated most advanced economies’ ordinary conduct in the international monetary system.

Chart 3.1.2 shows the proportions of monetary gold held by governments versus in private circulation. With this chart, we will confirm the paradigm transformation in the international monetary arrangement at the turn of the 20th century. This chart only covers the period 1845 to 1925, illustrating an overview of the transformation that took place between the Victorian Wave and the International Gold Standard Wave. Since this chart omits the bond wave chart, it accompanies signs to identify those periods.

This chart shows a notable gradual shift during the period in the proportion of monetary gold from the private sector to the vaults of the central government. At the early stage, this trend emerged and grew gradually along the international convergence into the gold standard.

As a background, the adoption of the gold standard by the Unified German Empire in 1871—with the massive amount of gold received from France as reparation after the Franco-Prussian War—created an advantage in network externality of the gold standard system in the international currency arrangement: many other major contemporary states gravitated toward the network externality of the gold standard. (Eichengreen, 2008, p. 17) This reflects the fact that an increasing number of monetary authorities began to find it necessary to accumulate gold to conduct the gold standard. (Green, 1999, p. 9)

Furthermore, the proportions of gold between the private sector and government cross at the turn of the century: more gold comes into the hands of monetary authorities. This almost coincides with the start of the international gold standard, reflecting the increasing importance of the gold reserve formation during the monetary system. The international convergence to the gold standard was completed with the US adoption of its gold standard in 1900. In terms of the international monetary regime, 1900 is a dividing point between two monetary epochs: the gradual international convergence to the gold standard from 1871 to 1900 and the international gold standard from 1900 to 1913. The monetary authorities’ affinity for gold continued to grow after 1900.

Around 1913, the level of gold circulating in the private sector starts collapsing. “While the gold standard was not officially suspended, in practice, it went into limbo.” (Green, 1999, p. 10) This almost coincides with the outbreak of WWI. To characterise the development, Timothy S. Green (1999) refers to John Clapham's remark: in a paraphrase, at the outbreak, the Bank of England acquired a massive amount of gold (over 500 m.t.) from South Africa and Australia and, while restricting gold export licensing from the UK, managed to absorb the gold from the market. The characteristics of the gold standard evolved together with the transformations in the circulation of monetary gold during WWI.

What we see in these two charts is a remarkable parallel in the rhythms between paradigm transformations in the international monetary regime and the bond wave: a compelling notion of synchronization between the bond wave and evolution in the international monetary regime, with some minor margin-of-time lags.

As a background, the adoption of the gold standard by the Unified German Empire in 1871—with the massive amount of gold received from France as reparation after the Franco-Prussian War—created an advantage in network externality of the gold standard system in the international currency arrangement: many other major contemporary states gravitated toward the network externality of the gold standard. (Eichengreen, 2008, p. 17) This reflects the fact that an increasing number of monetary authorities began to find it necessary to accumulate gold to conduct the gold standard. (Green, 1999, p. 9)

Furthermore, the proportions of gold between the private sector and government cross at the turn of the century: more gold comes into the hands of monetary authorities. This almost coincides with the start of the international gold standard, reflecting the increasing importance of the gold reserve formation during the monetary system. The international convergence to the gold standard was completed with the US adoption of its gold standard in 1900. In terms of the international monetary regime, 1900 is a dividing point between two monetary epochs: the gradual international convergence to the gold standard from 1871 to 1900 and the international gold standard from 1900 to 1913. The monetary authorities’ affinity for gold continued to grow after 1900.

Around 1913, the level of gold circulating in the private sector starts collapsing. “While the gold standard was not officially suspended, in practice, it went into limbo.” (Green, 1999, p. 10) This almost coincides with the outbreak of WWI. To characterise the development, Timothy S. Green (1999) refers to John Clapham's remark: in a paraphrase, at the outbreak, the Bank of England acquired a massive amount of gold (over 500 m.t.) from South Africa and Australia and, while restricting gold export licensing from the UK, managed to absorb the gold from the market. The characteristics of the gold standard evolved together with the transformations in the circulation of monetary gold during WWI.

What we see in these two charts is a remarkable parallel in the rhythms between paradigm transformations in the international monetary regime and the bond wave: a compelling notion of synchronization between the bond wave and evolution in the international monetary regime, with some minor margin-of-time lags.

Salient Features

Returning to Chart 3.1.1, another salient feature pertains to amplification of the post–WWII bond waves, both in terms of time horizon and in magnitude: larger swings in the Reconstruction Wave and the Globalization Wave, in comparison with the International Gold Standard Wave and the Vacuum Wave. This amplification coincides with the monetary transformation to fiat money, as if the former were a manifestation of the latter.

It is compelling to speculate that the gradual shift to the fiat money system is one of the factors that contributed to the amplification in the post–WWII bond waves’ larger swing. As the restraint of metallic conversion loosened gradually, its impact on the price became inflationary; hence, it manifested in amplified swings in the magnitude of bond yields. At the same time, unconstrained by the widely presumed automatic corrective mechanism of the gold standard, discretionary government interventions might well have extended the time horizon of the post–WWII bond waves. These intuitive notions suggest that the monetary regime change might have exerted a great impact on the bond wave through the evolution of inflation.

These manifestations, mirrored in the bond wave, imply that the dynamics of modern floating- exchange-rates fiat-money distinguishes itself both in quality and quantity from the fixed exchange rates regime of the metallic standards.

It is compelling to speculate that the gradual shift to the fiat money system is one of the factors that contributed to the amplification in the post–WWII bond waves’ larger swing. As the restraint of metallic conversion loosened gradually, its impact on the price became inflationary; hence, it manifested in amplified swings in the magnitude of bond yields. At the same time, unconstrained by the widely presumed automatic corrective mechanism of the gold standard, discretionary government interventions might well have extended the time horizon of the post–WWII bond waves. These intuitive notions suggest that the monetary regime change might have exerted a great impact on the bond wave through the evolution of inflation.

These manifestations, mirrored in the bond wave, imply that the dynamics of modern floating- exchange-rates fiat-money distinguishes itself both in quality and quantity from the fixed exchange rates regime of the metallic standards.

Returning to Chart 3.1.1, another salient feature pertains to amplification of the post–WWII bond waves, both in terms of time horizon and in magnitude: larger swings in the Reconstruction Wave and the Globalization Wave, in comparison with the International Gold Standard Wave and the Vacuum Wave. This amplification coincides with the monetary transformation to fiat money.

It is compelling to speculate that the gradual shift to the fiat money system is one of the factors that contributed to the amplification in the post–WWII bond waves’ larger swing. As the fetter of metallic conversion loosened gradually, its impact on the price became inflationary; hence, it manifested in amplified swings in the magnitude of bond yields. At the same time, unconstrained by the widely presumed automatic corrective mechanism of the gold standard, discretionary government interventions might well have extended the time horizon of the post–WWII bond waves. These intuitive notions suggest that the monetary regime change might have exerted a great impact on the bond wave through the evolution of inflation.

These manifestations, mirrored in the bond wave, imply that the dynamics of modern floating- exchange-rates-fiat-money distinguishes itself both in quality and quantity from the fixed exchange rates regime of the metallic standards.

It is compelling to speculate that the gradual shift to the fiat money system is one of the factors that contributed to the amplification in the post–WWII bond waves’ larger swing. As the fetter of metallic conversion loosened gradually, its impact on the price became inflationary; hence, it manifested in amplified swings in the magnitude of bond yields. At the same time, unconstrained by the widely presumed automatic corrective mechanism of the gold standard, discretionary government interventions might well have extended the time horizon of the post–WWII bond waves. These intuitive notions suggest that the monetary regime change might have exerted a great impact on the bond wave through the evolution of inflation.

These manifestations, mirrored in the bond wave, imply that the dynamics of modern floating- exchange-rates-fiat-money distinguishes itself both in quality and quantity from the fixed exchange rates regime of the metallic standards.

Looking to the Future:

Questions About the Forthcoming Paradigm Transformation

in the International Monetary System

Once again, milestones events associated with transformations in currency regime took place in extreme monetary conditions. We are presumably positioned the near bottom of the Globalization Wave, at least in terms of yield level, although timing remains uncertain at this point. If history is a guide, what can be anticipated for the future based on empirical cases?

- Can we find any precursor signalling a transformation in the international monetary paradigm?

- Flooded with massive liquidity by monetary expansion, can a fiat money regime sustain itself? Put it in Minsky’s terms—stability is destabilising—will artificial stability in the system be destabilising in the long term? That could lead to a breakdown of the current regime and a shift to a new regime that we have never experienced in our history.

- On the contrary, the current regime might manage to sustain and emerging economies might converge into the current floating currency regime. That would be another international convergence case analogous to the development during the Victorian Wave.

- Or, are we entering into a new currency regime that the world has never experienced in history—such as digital money?

Historical case outlines

If history is a guide, we should be able to extract some useful information from the empirical study. That said, since the future does not exist in the past—and we do reserve our power to shape the future differently from the past—here we need to incorporate new developments into analogy. As a matter of fact, there are variations in the nature of historical regime transitions. Here are some outlines of historical cases.

1) The Birth of British Gold Standard:

The British gold standard debuted against the deterministic intentions of the top mind of the monetary authority at that time, Isaac Newton (then Master of the Mint) in his defence of the UK’s existing bimetallic standard. It was the by-product of market participants’ victory over Newton’s rigidity toward the exchange rate. Newton undervalued silver relative to gold in determining the monetary value ratio between them. In response, arbitrageurs exported silver coins from the United Kingdom to benefit the price difference between the domestic market and abroad. As a result, silver coins disappeared from the United Kingdom around 1717. With only gold coins left, the bimetallic standard mutated to become the de facto gold standard. (Bernstein, 2000, pp. 195-197) As the founder of Newtonian Physics, Newton exerted his deterministic thinking in monetary management, where uncertainties dictate the consequences. In this case, market participants’ punishment of the monetary authority’s mismanagement led to the paradigm shift in currency regime. The new regime unfolded as a product of the failure of the previous regime: the gold standard was born as a mutant of the bimetallic standard. As a reminder, here is a remark by John Maynard Keynes about Isaac Newton: "Newton was not the first of the age of reason. He was the last of the magicians, the last of the Babylonians and Sumerians, the last great mind which looked out on the visible and intellectual world with the same eyes as those who began to build our intellectual inheritance rather less than 10,000 years ago." (Keynes, n.d.)

2) The international convergence to the gold standard:

The international convergence to the gold standard during the last quarter of the 19th century unfolded in an orderly and gradual fashion. The contemporary major economies gravitated toward the network externalities of the gold standard in a relatively orderly fashion. (Eichengreen, 2008, p. 17)

3) The break-down of the International Gold Standard:

In the case of the international gold standard, it took two bond waves— the Vacuum Wave and the Reconstruction Wave—for the world to abandon it and arrive at the new regime (floating exchange rates under fiat money). During those two bond waves, the two centres of gravity in the global economy—the United Kingdom and the United States—made abortive efforts to defend the legacy metallic regime.

During the inter-war period from 1918 to 1937, two counter-forces fight back and forth. On one hand, the Bank of England demonstrated a persistent, rigorous willingness to restore its pre-war monetary system of the gold standard. On the other, the market participants expressed (through arbitrage actions) their counter-opinion that the United Kingdom had lost the ability to do so. Throughout the UK’s experience during this period, the aforementioned caveat by Benjamin Disraeli resonates.

The new regime, the Bretton Woods System, waited for one whole bond bull wave to emerge. It was the de-facto USD standard in which only the USD was eligible for gold convertibility and all other currencies were loosely pegged to USD. The backdrop, the power vacuum of the post–WWII Old Continent and the context of the Cold War, enable the United States to dictate the course of the event in shaping the new regime.. Nevertheless, discontent was openely expressed by prominent contemporaries, such as John Maynard Keynes and Charles de Gaulle. Of note, Valery Giscard d’Estaing, the finance minister of the de Gaulle administration, called the asymmetric seigniorage power granted to the USD “exorbitant privilege.” (Eichengreen, 2011, p. 4)

Nevertheless, the series of events below brought fiat money system into being.

4) Uni-Polar Fiat Money Central Banker's Monetary Policy Standard:

Throughout the Globalization Wave, among major advanced economies fiat money has become operated in a floating exchange rate system with price stability foduced monetary policy managed by central bankers. It was also characterised by the dominance of USD as the global reserve currency: in other words, “Uni-Polar Fiat CBMPS System” under USD dominance.

Thereafter, throughout the Globalization Wave, among major advanced economies fiat money has become operated in a floating exchange rate system with price stability foduced monetary policy managed by central bankers. It was also characterised by the dominance of USD as the global reserve currency: in other words, “Uni-Polar Fiat Money CBMPS System” under USD dominance.

The British gold standard debuted against the deterministic intentions of the top mind of the monetary authority at that time, Isaac Newton (then Master of the Mint) in his defence of the UK’s existing bimetallic standard. It was the by-product of market participants’ victory over Newton’s rigidity toward the exchange rate. Newton undervalued silver relative to gold in determining the monetary value ratio between them. In response, arbitrageurs exported silver coins from the United Kingdom to benefit the price difference between the domestic market and abroad. As a result, silver coins disappeared from the United Kingdom around 1717. With only gold coins left, the bimetallic standard mutated to become the de facto gold standard. (Bernstein, 2000, pp. 195-197) As the founder of Newtonian Physics, Newton exerted his deterministic thinking in monetary management, where uncertainties dictate the consequences. In this case, market participants’ punishment of the monetary authority’s mismanagement led to the paradigm shift in currency regime. The new regime unfolded as a product of the failure of the previous regime: the gold standard was born as a mutant of the bimetallic standard. As a reminder, here is a remark by John Maynard Keynes about Isaac Newton: "Newton was not the first of the age of reason. He was the last of the magicians, the last of the Babylonians and Sumerians, the last great mind which looked out on the visible and intellectual world with the same eyes as those who began to build our intellectual inheritance rather less than 10,000 years ago." (Keynes, n.d.)

2) The international convergence to the gold standard:

The international convergence to the gold standard during the last quarter of the 19th century unfolded in an orderly and gradual fashion. The contemporary major economies gravitated toward the network externalities of the gold standard in a relatively orderly fashion. (Eichengreen, 2008, p. 17)

3) The break-down of the International Gold Standard:

In the case of the international gold standard, it took two bond waves— the Vacuum Wave and the Reconstruction Wave—for the world to abandon it and arrive at the new regime (floating exchange rates under fiat money). During those two bond waves, the two centres of gravity in the global economy—the United Kingdom and the United States—made abortive efforts to defend the legacy metallic regime.

During the inter-war period from 1918 to 1937, two counter-forces fight back and forth. On one hand, the Bank of England demonstrated a persistent, rigorous willingness to restore its pre-war monetary system of the gold standard. On the other, the market participants expressed (through arbitrage actions) their counter-opinion that the United Kingdom had lost the ability to do so. Throughout the UK’s experience during this period, the aforementioned caveat by Benjamin Disraeli resonates.

The new regime, the Bretton Woods System, waited for one whole bond bull wave to emerge. It was the de-facto USD standard in which only the USD was eligible for gold convertibility and all other currencies were loosely pegged to USD. The backdrop, the power vacuum of the post–WWII Old Continent and the context of the Cold War, enable the United States to dictate the course of the event in shaping the new regime.. Nevertheless, discontent was openely expressed by prominent contemporaries, such as John Maynard Keynes and Charles de Gaulle. Of note, Valery Giscard d’Estaing, the finance minister of the de Gaulle administration, called the asymmetric seigniorage power granted to the USD “exorbitant privilege.” (Eichengreen, 2011, p. 4)

Nevertheless, the series of events below brought fiat money system into being.

- In 1971, the United States abolished the system of its own making, the Bretton Woods System, when Richard Nixon, then president of the United States, succumbed to market pressures and announced the unilateral abolition of the USD’s gold convertibility.

- Between 1979-1981, Paul Volcker, then-Chairman of the Federal Reserve Bank, took a decisive monetary policy to contain inflation through federal rate hike. Volcker’s inflation fight led to the reversal of the bond wave. Volcker's move during 1979-1981 was a strong political announcement that the new monetary regime, fiat money, needs to be managed by central bankers with a special attention to price stability. In other words, the new monetary regime is not merely fiat money, but also "Central Banker's Monetary Policy Standard (CBMPS)."

4) Uni-Polar Fiat Money Central Banker's Monetary Policy Standard:

Throughout the Globalization Wave, among major advanced economies fiat money has become operated in a floating exchange rate system with price stability foduced monetary policy managed by central bankers. It was also characterised by the dominance of USD as the global reserve currency: in other words, “Uni-Polar Fiat CBMPS System” under USD dominance.

Thereafter, throughout the Globalization Wave, among major advanced economies fiat money has become operated in a floating exchange rate system with price stability foduced monetary policy managed by central bankers. It was also characterised by the dominance of USD as the global reserve currency: in other words, “Uni-Polar Fiat Money CBMPS System” under USD dominance.

Looking back, the monetary authorities of the past showed a notable tendency towards inertia in resisting forthcoming change. They often, if not always, positioned themselves in defence of the old regime. The actual transformation was often driven by the psychology of market participants: they often punished the authority’s mismanagement through arbitrage transactions. Below I categorize these empirical regime changes into three classifications. Even if this list might not be the comprehensive classification of paradigm shift in currency regime, it might provide us with some insight when we contemplate the future regime shift.

Overall, the modern international monetary system evolved from a fixed exchange rate regime under metallic money to a floating exchange regime under fiat money.

- A regime change can be driven by political choice of the power state. In such a case, the new regime is designed to best serve the interest of power states: often its design compromises certain economic principles that are required to serve as an optimal international monetary system. The result would be an asymmetric system, which causes a great inconvenience to peripheries. The designing of Bretton Woods might fall into this classification.

- A regime change can be driven by the flaw in the design of an existing currency regime in place. Three empirical examples can illustrate such a case:

- Isaac Newton’s story: his bimetallic standard was mutated into a gold standard, when Newton mispriced silver-gold ratio.

- The failure of the gold standard during the Vacuum Wave: the rigid gold conversion rate failed to reflect the weakened economic capacity of the United Kingdom.

- The failure of the Bretton Woods System: fixed rate arrangement did not serve the fluid dynamics of the reconstruction efforts.

- Isaac Newton’s story: his bimetallic standard was mutated into a gold standard, when Newton mispriced silver-gold ratio.

- A regime change can be driven by external factors: It was a by-product of the geopolitical conflict in the Europe that accounted for the international convergence to the gold standard during the late 19th Century. With the United Kingdom staying out of the geopolitical conflict, its gold standard was the only functioning sizeable currency regime. The united German state chose to abandon its old currency regime, silver standard, and participate into the gold standard, resulting in the network externality of the gold standard. The rest of the advanced economies followed the suites.

Overall, the modern international monetary system evolved from a fixed exchange rate regime under metallic money to a floating exchange regime under fiat money.

What would be the next evolution?

When we study the problems in the current monetary system, some hints for the answer may emerge. Faced with deflationary pressure in the post-Global Financial Crisis period, some monetary authorities have been compelled to apply negative interest rates.

Under the current fiat money system, central banks are constrained by the zero boundary of interest rates and cannot apply negative interest rates universally: the scope of the use of negative interest rates so far was only limited to interbank transactions between regulated banks.

For that, money must be registered. Under the current fiat money, there is an economic division between cash hoarding at home and money saved at the bank, when negative interest rates are applied. Simply put, the former is free from negative interest rates, and the latter is not. Since savings are subject to a charge, negative interest rates, more people would likely hoard money at home to escape from the charge imposed on their saving. With a substantial decline in savings, banks would go out of business. In this sense, the fiat money system does not allow monetary authorities to apply negative interest rates to saving accounts. It only enables them to enforce negative interest rates among regulated banks.

One solution is to digitize money. When money is digitized, it is registered; therefore, it can be universally subject to negative interest rates. There are both proponents and opponents for the “go digital” option.

As an example of an opposing view, some argue that governments would lose their seigniorage abilities if they introduced digitized money. However, there is a new reality emerging. To contain corruption, India announced a drastic measure to abolish high-denomination bank notes. (Bloomberg, 2016) (The public is still allowed to use credit cards and bank transfers for large transactions.) This is one step towards digital money.

Another speculation that supports digital money comes from the issue of money laundering. There is speculation that other countries, such as Singapore and China, are considering introducing digital money to crack down on money laundering and corruption. (Bloomberg, 2016) One question is whether legislators can achieve any consensus on digital money: political pressure from corrupted legislators must be enormous.

Another question is, what if, when money goes digitize? Although less fungible, there remain other means for those corrupted to conceal illegitimate transactions from the government radar: barter or quid pro quo. Among them, gold might be the most fungible example. In that case, the black market would end up reintroducing the metallic standard—in other words, “back to antiquity.” The world could enter a multi-standard currency regime if digital money is introduced.

Under the current fiat money system, central banks are constrained by the zero boundary of interest rates and cannot apply negative interest rates universally: the scope of the use of negative interest rates so far was only limited to interbank transactions between regulated banks.

For that, money must be registered. Under the current fiat money, there is an economic division between cash hoarding at home and money saved at the bank, when negative interest rates are applied. Simply put, the former is free from negative interest rates, and the latter is not. Since savings are subject to a charge, negative interest rates, more people would likely hoard money at home to escape from the charge imposed on their saving. With a substantial decline in savings, banks would go out of business. In this sense, the fiat money system does not allow monetary authorities to apply negative interest rates to saving accounts. It only enables them to enforce negative interest rates among regulated banks.

One solution is to digitize money. When money is digitized, it is registered; therefore, it can be universally subject to negative interest rates. There are both proponents and opponents for the “go digital” option.

As an example of an opposing view, some argue that governments would lose their seigniorage abilities if they introduced digitized money. However, there is a new reality emerging. To contain corruption, India announced a drastic measure to abolish high-denomination bank notes. (Bloomberg, 2016) (The public is still allowed to use credit cards and bank transfers for large transactions.) This is one step towards digital money.

Another speculation that supports digital money comes from the issue of money laundering. There is speculation that other countries, such as Singapore and China, are considering introducing digital money to crack down on money laundering and corruption. (Bloomberg, 2016) One question is whether legislators can achieve any consensus on digital money: political pressure from corrupted legislators must be enormous.

Another question is, what if, when money goes digitize? Although less fungible, there remain other means for those corrupted to conceal illegitimate transactions from the government radar: barter or quid pro quo. Among them, gold might be the most fungible example. In that case, the black market would end up reintroducing the metallic standard—in other words, “back to antiquity.” The world could enter a multi-standard currency regime if digital money is introduced.

Reference

- Bernstein, P. L. (2000). The power of gold: the history of an obsession. New York: John Wiley & Sons, Inc.

- Carter et al. (2006). Historical statistics of the United States : earliest times to the present (Millenium Ed. ed.). (S. B. Carter, Ed.) New York, NY: Cambridge University Press.

- Eichengreen, B. (2008). Globalizing capital: a history of the international monetary system (Second edition ed.). Princeton University Press.

- Eichengreen, B. (2011). Exorbitant Privilege. Oxford: Oxford University Press.

- Green, T. S. (1999). Central Bank Gold Reserves: a historical perspective since 1845. London: World Gold Council.

- Keynes, J. M. (n.d.). Newton, the man. Retrieved from http://phys.columbia.edu/~millis/3003Spring2016/Supplementary/John%20Maynard%20Keynes_%20%22Newton,%20the%20Man%22.pdf

Copyright © 2016 by Michio Suginoo. All rights reserved.